Can Anyone Become a Company Director in the UK?

Can Anyone Become a Company Director in the UK?

Becoming a company director in the UK may appear relatively straightforward, particularly as companies can now be incorporated quickly online. However, acting as a director involves far more than simply holding a title.

Directors are overseeing for managing a company’s affairs and are subject to a range of legal duties and obligations under the Companies Act 2006. Understanding these responsibilities is essential before accepting an appointment as a director.

Who Can Become a Company Director?

In the UK, most individuals can become a company director provided they meet certain legal requirements. A director must generally:

- Be at least 16 years old

- Not be disqualified from acting as a director

- Not be subject to a bankruptcy restrictions order or equivalent restrictions

- Have consented to act as a director

There is no requirement for a director to be a UK citizen, live in the UK, or hold professional qualifications. As a result, many UK companies have overseas directors and international business owners.

However, regardless of where a director lives, UK companies must continue to comply with their legal obligations, including maintaining a registered office, filing documents with Companies House, and meeting any applicable UK tax requirements.

What Does a Company Director Actually Do?

A director is responsible for managing the company and making decisions in its best interests.

This may include:

- Managing day-to-day business operations

- Entering into contracts

- Overseeing finances

- Ensuring legal and regulatory compliance

- Making strategic business decisions

- Acting in the best interests of the company

The precise authority of directors is often governed by the company’s articles of association and any shareholders’ agreement that may be in place.

Legal Duties of Directors

Under sections 171–177 of the Companies Act 2006, directors owe statutory duties to the company.

These duties include obligations to:

- Act within their powers

- Promote the success of the company

- Exercise independent judgment

- Exercise reasonable care, skill and diligence

- Avoid conflicts of interest

- Not accept benefits from third parties

- Declare interests in proposed transactions or arrangements

These duties apply regardless of whether the director is actively involved in the daily running of the business.

Can Directors Be Personally Liable?

Although a company is a separate legal entity, directors may in certain circumstances face personal liability.

Examples may include:

- Breach of directors’ duties

- Wrongful or fraudulent trading

- misapplication of company assets

- Certain statutory or regulatory breaches

In serious cases, directors may also face disqualification proceedings under the Company Directors Disqualification Act 1986.

Why Legal Advice Matters

Many business owners accept director appointments without fully understanding the legal responsibilities involved.

Seeking legal advice at an early stage can help directors:

- Understand their duties

- Reduce governance risks

- Ensure proper decision-making procedures are followed

- Protect the interests of the company

- Minimise the risk of disputes or liability

This is particularly important for start-ups, family businesses, shareholder-managed companies, and businesses with overseas elements.

How We Can Help

At Chan Neill Solicitors LLP, our corporate and commercial team advises directors, shareholders, investors, and businesses on a wide range of company law and corporate governance matters.

If you require advice regarding directors’ duties, shareholder relationships, company governance, or corporate disputes, our team would be pleased to assist.

Shareholder vs Director: What’s the Difference?

In many UK companies, particularly smaller or owner-managed businesses, the terms “shareholder” and “director” are often used interchangeably. However, they perform very different roles within a company.

Understanding the distinction between shareholders and directors is essential when dealing with company governance, decision-making, legal responsibilities, and shareholder disputes.

Shareholders

A shareholder is an owner of the company. Shareholders hold shares in the business and may benefit from the company’s success through dividends or an increase in share value.

Depending on the type and number of shares they hold, shareholders may also have voting rights on important company matters.

Shareholders are not usually responsible for the day-to-day management of the company. Instead, they generally exercise influence through ownership rights and voting powers.

Directors

A director, on the other hand, is responsible for managing the company’s affairs and day-to-day operations.

Directors make strategic and operational decisions on behalf of the company. This may include:

- entering into contracts;

- managing employees;

- overseeing finances;

- ensuring regulatory compliance; and

- acting in the company’s best interests.

Directors owe legal duties to the company under the Companies Act 2006, including duties to:

- act within their powers;

- promote the success of the company;

- avoid conflicts of interest; and

- exercise reasonable care, skill and diligence.

Can Someone Be Both a Shareholder and Director?

Yes. In many private companies, particularly family businesses and start-ups, the same individual may act as both a shareholder and a director.

However, ownership and management remain legally distinct concepts.

For example:

- a shareholder owns part of the company;

- a director manages the company.

An individual acting in both capacities should understand the separate rights and responsibilities attached to each role.

A clear understanding of the distinction between shareholders and directors can help businesses maintain effective corporate governance and reduce the risk of internal disputes.

At Chan Neill Solicitors LLP, our corporate and commercial team advises businesses, directors, and shareholders on a wide range of company law matters, including shareholder agreements, directors’ duties, and corporate disputes.

Can You Remove a Director for Breaching Their Duties?

The Directors’ Duties Series – Part 2

In our previous article on acting within powers, we introduced one of the key duties owed by directors under UK law.

All company directors must comply with the duties set out in Chapter 2 of Part 10 of the Companies Act 2006.

These duties include:

- Acting within powers

- Promoting the success of the company

- Exercising independent judgment

- Exercising reasonable care, skill and diligence

- Avoiding conflicts of interest

- Not accepting benefits from third parties

- Declaring any interest in a proposed transaction or arrangement

But what happens if a director breaches these duties?

Under English law, limited companies are generally free to determine their own internal governance. As a result, the appropriate route for removing a director will often depend on the company’s specific constitutional and contractual arrangements.

In practice, identifying the correct procedure is not always straightforward, and missteps can lead to disputes or legal challenges. Even where company documents do not provide a clear mechanism, shareholders may still rely on statutory rights under the Companies Act 2006 to remove a director.

Statutory Right of Removal: Procedure and Key Considerations

Under section 168 of the Companies Act 2006, a director can be removed by an ordinary resolution (more than 50% of shareholder votes).

However, strict procedural requirements must be followed including serving special notice must be given (at least 28 days before the meeting), the director must be informed of the proposed removal, has the right to make written representations and given the opportunity to speak at the meeting.

Failure to follow the correct procedure may render the removal invalid.

Breach of Duties and Shareholder Remedies

A breach of directors’ duties does not automatically result in removal, but it can give rise to legal action.

Shareholders may consider:

- Derivative claims

Shareholders may bring a claim on behalf of the company against a director for breach of duty, negligence, or misconduct. - Unfair prejudice petitions (section 994)

Where a director’s conduct unfairly prejudices shareholders’ interests, members may apply to the court for relief.

These remedies are particularly relevant in more serious or contested disputes.

Removing a director is rarely just a procedural step and can involve wider legal and commercial issues. For example:

- The director may also be an employee, giving rise to potential employment law risks, including claims for unfair or wrongful dismissal

- There may be contractual implications under any service agreement or shareholder arrangements

- Disputes can escalate quickly, particularly in closely held or family-run companies

Why Legal Advice Is Important

In light of these overlapping issues, taking legal advice at an early stage can be critical. It helps ensure the correct procedure is followed, manage potential risks, and reduce the likelihood of disputes or costly challenges.

Conclusion

While UK law provides a mechanism for removing a director, the appropriate approach will depend on the company’s governing documents and the specific circumstances. Starting with the company’s Articles of Association, together with taking legal advice where appropriate, can help ensure the process is carried out smoothly and in a legally compliant manner.

At Chan Neill Solicitors LLP, our Corporate and Litigation teams advise on director duties, shareholder disputes, and wider company governance matters, and are well placed to assist with issues arising from the removal of a director.

Acting Within Powers: Why Your Company’s Rulebook Matters

The Directors’ Duties Series – Part 1

When Annie joined the board of a growing fintech start-up, she didn’t think much about the company’s Articles of Association. After all, wasn’t that just “boilerplate” paperwork filed years ago?

That assumption cost her.

Months later, Annie approved a new share issue to an investor - a move later challenged by other shareholders. The problem? The Articles required both board approval and a special shareholder resolution, which she hadn’t obtained.

The court found she had acted outside her powers under section 171 of the Companies Act 2006. The share issue was set aside, and Annie faced a claim by the company for breach of duty.

What Does Section 171 Require?

Directors must:

- Act in accordance with the company’s constitution, which includes the Articles of Association and certain formal resolutions, and may also operate alongside other governance documents such as shareholders’ agreements; and

- Only exercise their powers for the purposes for which those powers were conferred.

It sounds straightforward, yet this duty is frequently overlooked, particularly in fast-moving companies where “commercial urgency” tends to trump formalities. But failing to check your authority before taking key decisions can unravel months of work, create shareholder disputes, and expose directors personally to claims.

How to Stay Compliant

- Know your rulebook - Regularly check your company’s constitution before important decisions: issuing shares, signing material contracts, restructuring the company, approving major transactions, or any action that might require shareholder consent.

- Document your authority - Ensure that minutes and resolutions clearly record board decisions.

- Seek early advice - If you’re unsure, take legal guidance before acting, particularly where the Articles or shareholders’ agreements contain bespoke provisions. It is far easier to confirm authority than to unwind an unauthorised decision.

Directors who understand where their powers begin and end not only protect themselves, they build credibility and trust in the boardroom.

How We Can Help

At Chan Neill Solicitors LLP, we regularly advise company directors, boards, and shareholders on governance, compliance, and risk management under UK company law and related legislation.

If you are uncertain about the scope of your powers or other obligations as a director, or wish to review your company’s governance framework, Articles, board procedures, shareholders’ agreements, or compliance processes, our corporate team can advise on practical steps to ensure you meet your duties and manage risk effectively.

Get in touch with us to discuss how we can help you and your business.

Next in the series:

Promoting the Success of the Company (s.172) - balancing the company’s success with wider stakeholder interests.

Disclaimer:

This publication is intended for general information purposes only and does not constitute legal or professional advice. You should not act upon the information contained in this article without obtaining specific legal advice. Chan Neill Solicitors LLP accepts no responsibility for any loss which may arise from reliance on information contained herein.

Business Restructuring: Navigating Challenges and Opportunities in 2025

As we step into 2025, UK businesses face a multifaceted landscape. With the Office for Budget Responsibility (OBR) projecting a 2% economic growth, there are signs of progress. However, companies must navigate a range of challenges and seize emerging opportunities to thrive. Here, we explore the key trends shaping business restructuring in 2025 and practical strategies for success.

The Economic Picture

The economic outlook for 2025 presents a mixed picture. While there are some forward movements, businesses face a challenging environment due to several factors:

- Increased employer National Insurance contributions

- Rising national minimum wage rates

- New packaging levies & taxes

- Elevated business rates

These factors are making operations more expensive for businesses. Additionally, many firms continue to grapple with the lingering effects of past inflation and high interest rates, which strain cash flow and impact financial resilience.

Key Challenges

Property Market Stress

The commercial real estate sector is expected to face ongoing distress, driven by compressed valuations and liquidity constraints. This environment may prompt companies to restructure their real estate portfolios, renegotiate leases, and address debt obligations tied to property assets.

Debt Management

Liability management transactions are anticipated to rise in the European market, including the UK. However, these transactions may not reach the prevalence seen in the US due to factors like sponsor caution, family-owned business hesitations, and the complexities of navigating multiple jurisdictions across Europe.

Regulatory Changes

From 14 May, 2025, insolvency practitioners will be subject to new sanctions reporting obligations. This regulatory shift will require professionals to adjust their practices and ensure compliance with evolving legal standards. Businesses undergoing restructuring must remain vigilant to stay ahead of these changes.

Employment Law Adjustments

Potential changes to employment laws, particularly around collective redundancy rules, could pose significant challenges for companies in distress. Navigating these changes will demand careful planning to ensure compliance while safeguarding business recovery efforts.

Skills Shortage

The persistent skills shortage continues to challenge businesses, particularly those undergoing restructuring. Companies must rethink their recruitment strategies, enhance employee development initiatives, and foster workplace cultures that prioritize flexibility and well-being to attract and retain top talent.

Strategies for Success

While the challenges are considerable, businesses can adopt proactive strategies to position themselves for success:

- Stay informed. Keep abreast of evolving case law and legal precedents, particularly in sectors experiencing significant restructuring activity

- Ensure Regulatory Compliance. Adapt to new regulatory requirements, such as the sanctions reporting obligations for insolvency practitioners, to avoid potential legal and financial repercussions.

- Focus on Sustainability. Develop comprehensive sustainability strategies to meet increasing environmental expectations and enhance business resilience.

- Address Skills Gaps. Invest in targeted recruitment efforts, employee training programs, and initiatives that create an appealing workplace culture.

- Maintain Financial Flexibility. Diversify revenue streams and establish robust financial management practices to mitigate economic uncertainties.

The business landscape in 2025 presents both challenges and opportunities. Companies that proactively adapt to regulatory changes, prioritize compliance, and adopt innovative strategies will be well-positioned to navigate the complexities of restructuring. By staying informed and embracing flexibility, UK businesses can overcome obstacles and unlock new avenues for growth.

If your business is considering restructuring or requires guidance on navigating these challenges, our team of legal experts is here to help. Contact us today to learn more about how we can support your journey through 2025 and beyond.

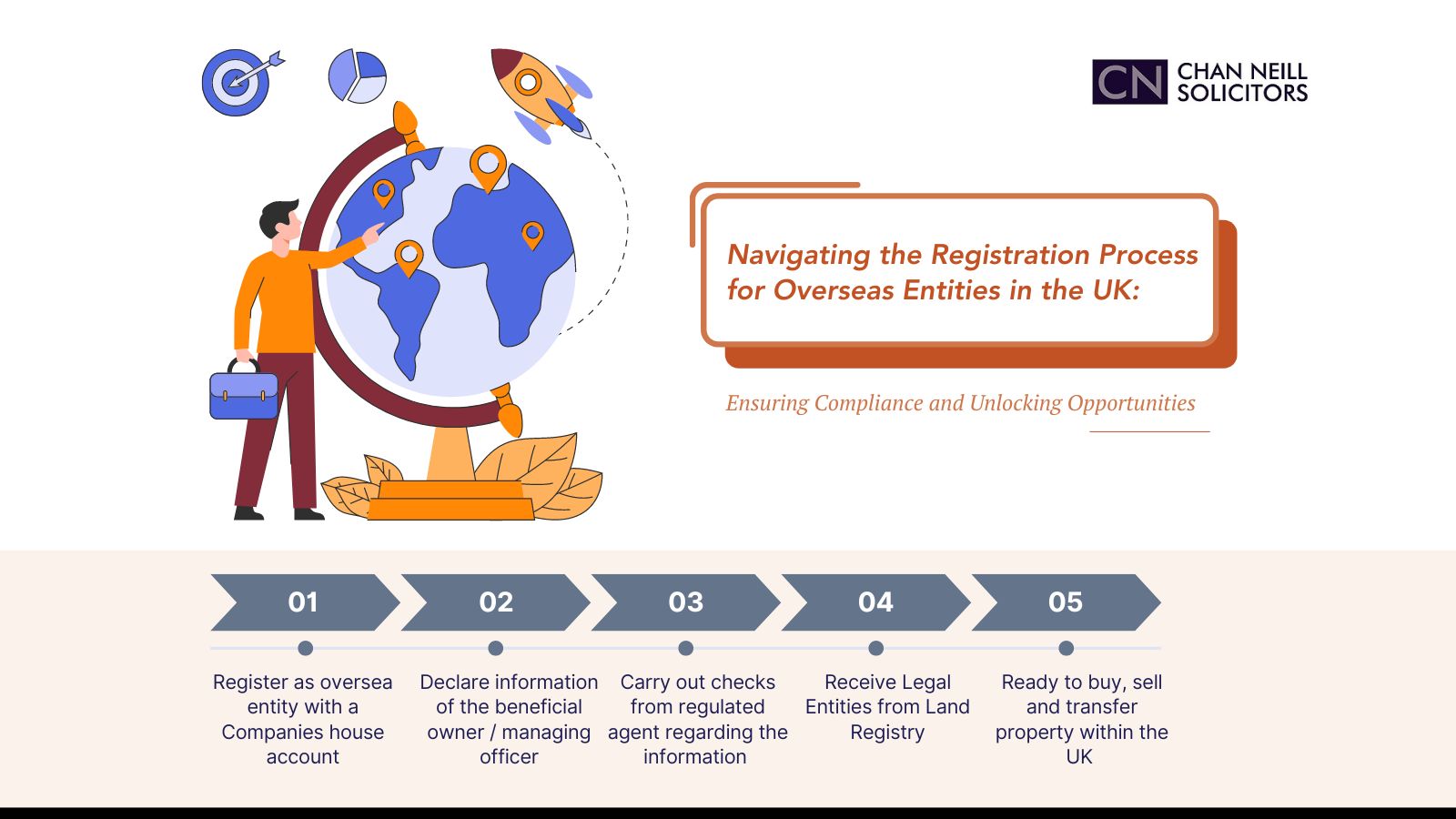

Navigating the Registration Process for Overseas Entities in the UK: Ensuring Compliance and Unlocking Opportunities

The UK continues to attract businesses from all corners of the globe. With its business-friendly infrastructure, environment and history, the UK remains a top destination for international entities seeking to establish a presence. However, for overseas companies looking to operate within the UK, navigating the regulatory landscape can be a daunting task.

One crucial step in this process is the registration of overseas entities, a procedure designed to ensure transparency, accountability, and compliance with UK laws. The Register of Overseas Entities (RoE) was established by the Economic Crime (Transparency and Enforcement) Act 2022 (ECTEA). It is regarded as an important step in dealing with global economic crime and furthering legitimacy within the UK property market.

The registration of overseas entities in the UK falls under the control of the Companies House, the government agency responsible for maintaining the official register of companies in the UK. Overseas entities seeking to establish a presence in the UK have historically had to register as an 'overseas company' if they plan to carry out business activities within the jurisdiction. On 26 October 2023, the ECTEA received Royal Assent, meaning that overseas entities which own UK property or land must declare information regarding their beneficial owners and/or managing officers.

To apply to register an overseas entity and its beneficial owners, the entity will require a Companies House Account. Detailed information about the overseas entity is required and its beneficial owners and/or managing officers will need to supply information about any relevant trusts, alongside the registration fee. A UK regulated agent based in the UK, often a law firm such as ourselves, must also confirm that they have carried out the requisite verification checks on the information regarding the beneficial owners and/or managing officers. It is therefore quicker and easier for the UK regulated agent to carry out the registration process themselves.

While the registration process may seem complex at first glance, it offers several benefits for overseas entities seeking to establish a foothold in the UK property market.

Legal Recognition: Registration as an overseas company provides legal recognition and legitimacy, enhancing the entity's credibility and reputation in the UK market.

Access to Markets and Opportunities: Registered overseas entities gain access to the vast UK market and can capitalise on business opportunities, partnerships, and investments within the country.

Enhanced Transparency and Compliance: By registering with Companies House, overseas entities demonstrate their commitment to transparency and compliance with UK laws and regulations, fostering trust among stakeholders and potential partners. If Companies have made an error in applications or have been delayed in registering, a concerted effort to communicate reasoning with Companies House should still be appreciated as a commitment to the transparency and compliance the ECTEA intended.

Protection of Rights and Interests: Registration affords overseas entities legal protections and safeguards their property within the UK, including the ability to sell, buy and lease the properties as well as resolve disputes surrounding the properties through the British legal system.

Once the entity has registered with Companies House, it will be issued with an overseas entity ID number (OEID). When the entity then enters property transactions, this number will be supplied to the Land Registry. The entity will then be able to buy, sell and transfer property within the UK whilst satisfying the regulatory requirements.

In an increasingly interconnected world, the registration of overseas entities in the UK serves as a gateway for foreign companies to new opportunities. While the process may involve complexities and regulatory requirements, it offers numerous benefits for businesses looking to expand their operations into the UK and its property market.

This article is provided for general information only. It is not intended to be and cannot be relied upon as legal advice or otherwise. If you would like to discuss any of the matters covered in this article, please contact us using the contact form or email us on reception@cnsolicitors.com

How will new immigration rules affect international students and their families studying in the UK?

On 17th July 2023, the Home Office made some changes to immigration rules, the most significant of which is the restriction on overseas students bringing family members to the UK.

However, when the news was released in May, the Home Office announced the scheme expected to be implemented in January next year.

Unexpectedly, yesterday's Immigration Rules Update document announced without warning that the restriction on overseas students bringing family members had begun.

Today's post will focus on how this update to the immigration rules will affect overseas students.

Restrictions on student visa holders bringing family members to the UK.

The UK is home to several world-renowned institutions of higher education. Hence, so many international students from all over the world come to the UK every year to further their studies.

Students of all ages come to the UK for higher education, with many returning to study after starting a family. To allow students to combine family life with study, the UK government has previously allowed holders of long-term student visas to bring their spouses and children to the UK.

Whilst student visa holders are subject to restrictions on working hours and other business activities, their spouses are free to work and do business in the UK whilst on a Dependent visa. As a result, more and more people are using the combination of a student visa and a Dependent visa as a transition for the whole family to immigrate to the UK, which has led to the student visa being gradually abused and losing its original purpose.

This immigration rule update is also the result of the UK government's desire to stop the abuse of student visas and return them to their original purpose of serving academic research.

Overall, the Home Office has not applied a blanket rule on overseas students bringing family members with them. Instead, they have increased the requirements for overseas students who can bring family members with them, depending on the circumstances.

Currently (after 17th July) there are specific conditions for students to be able to bring their families to the UK:

- Government Scholarship students studying a programme of 6 months or more

- Full-time students studying a postgraduate or above programme (RQF level 7 or above) of 9 months or more.

Please note that the requirements will remain in effect until the end of this year, except for government scholarship students who will not be affected. Additionally, restrictions for students pursuing postgraduate or higher-level courses will be further strengthened starting from 1 January, 2024.

Only the following two types of postgraduate or above courses commencing after 1/1/2024 will be allowed to bring dependents:

- PHD doctoral degree or other doctoral degree (RQF level 8)

- Research-based Higher Degree (RQF 8)

This update to the immigration rules is only for upcoming dependents of students, and applications for dependents of students submitted before 17 July will be reviewed under the previous rules.

Pathway requirements added for a student visa to other work/business visas. Some new prerequisites for student visas to be converted to other work/business visas have been added to the Immigration Rules Update published on the 17th.

The work/business visas affected are:

- Skilled worker visas

- Visas within the Global Business Mobility Programme

- Tier 2 Minister of Religion Visa

- Overseas Chief Representative Visa

- British Ancestor Visa

- Global Talent Visa

- High Potential Talent Visa

- Expansion Worker Scale-up Visa

- Innovation Founder Visa

- International Athlete Visa

- Various short-term work visas, etc.

There were no special requirements in the previous immigration rules for converting a student visa to another work/business visa. If the student found a company with employer sponsorship qualification that is willing to sponsor him/her for the corresponding work visa or fulfilled the eligibility criteria for a particular business visa, then the student could convert to the corresponding visa at any time during his/her student visa.

However, with effect from yesterday (17 July), one of the following conditions must be met to be able to convert from a student visa to a work/business visa:

(a)The applicant must have completed the course of study for which the Confirmation of Acceptance for Studies was assigned (or a course to which ST 27.3 of Appendix Student applies); or

(b) Condition B:

(i) The applicant must be studying a full-time course of study at degree level or above with a higher education provider which has a track record of compliance; and

(c) Condition C:

(i) The applicant must be studying a full-time course of study leading to the award of a PhD with higher education provider which has a track record of compliance.

(ii) The Certificate of Sponsorship in SW 1.2(d) must have a start date no earlier than 24 months after the start date of that course.''.

The requirements for Global Talent Visa, High Potential Talent Visa and Innovative Founder Visa are more stringent, and only applicants who fulfil point 1 or 3 of the above conditions can complete the conversion from student visa to these 3 types of visas.

These are the highlights of this immigration rule update on the overseas student community. There is no restriction on international students to stay in the UK after graduation. If they cannot immediately convert from a student visa to a work or business visa, they can still obtain a two-year stay on a Graduate Visa and look for work opportunities in the UK. These measures are to prevent the misuse of student visas, work, or business visas, and to regulate the influx of immigrants to the UK. Additionally, they aim to enhance the overall quality of immigration.

Students undertaking advanced academic education and research in the UK will still be able to enjoy the right to bring their dependents with them, and the threshold between student and work/business visas will go some way to improving the quality of professional or business immigration.

Under the current criteria, if you wish to save time by completing a seamless transition from a student visa to a work or business visa to achieve permanent residence, we recommend you start your immigration pathway planning as early as possible.

The professional immigration team at Chan Neill Solicitors can provide you with the most suitable immigration solution based on your background. If you require any assistance, kindly reach out to us.

Illegal entry into the UK can harm your chances of getting permanent residence or citizenship

On 20 July 2023 the Illegal Migration Act 2023 received Royal Assent. Under the new Act, migrants who entered the UK illegally after 7 March 2023 will be barred from re-entering the UK or gaining residence or citizenship, and the ban will also apply to their UK-born children. The UK government will have a duty to refuse to process any asylum claims they make and to return them to their home country or a safe third country where their asylum claims will be processed.

The purpose of the bill is to "prevent and deter illegal immigration, particularly through unsafe and illegal routes, by requiring the removal from the UK of certain persons who enter or arrive in the UK in breach of immigration controls".

There are exceptions to this ban, however, as illegal immigrants may be exempted if they can prove that they have come to the UK from "a country which complies with the United Nations Convention on Refugees and where their life and liberty are at risk". However, since most illegal immigrants enter the UK through EU countries such as France, none of which fulfil these conditions, the threshold for exemption is quite high.

The United Nations has warned that the Illegal Immigration Bill passed by the British Parliament is inconsistent with the country's obligations under international human rights and refugee law and sets a worrying precedent for the abrogation of asylum-related obligations, which could be followed by other countries, including in Europe, and which could have a negative impact on international refugees.

The professional immigration team at Chan Neill Solicitors can provide you with the most suitable immigration solution based on your background. If you require any assistance, kindly reach out to us.

Why is Anti Money Laundering Check So Important?

On October 28 2021, the National Crime Agency (NCA) announced that they had filed civil claims against a Chinese mother and two sons in the name of suspected money laundering, and successfully asked them to hand over a London property worth 1.6 million pounds for compensation.

National Crime Agency (NCA) is a law enforcement agency in the UK. This agency is the UK’s leading agency in combating criminal groups. It mainly combats organised crime and economic crime, including human trafficking, weapons and drugs, cybercrime, as well as economic crime across regional and international borders etc.

A woman named Mrs Hajiyeva was previously investigated by The National Crime Agency, they issued her an "Unidentified Wealth Order" (UWO) and asked her to explain and prove the source of her large amount of funds. The lady was unable to explain the legal source of her funds, thus, the National Crime Agency confiscated her luxury house in London.

What is the "Unidentified Wealth Order" (UWO)?

UWO refers to "Unexplained Wealth Order", which is a court order issued by a British court to enable the target person to disclose the unknown source of wealth. The relevant requirement for issuing an "unknown wealth order" is that the court must be convinced that there are reasonable grounds to suspect that the target person's known legal source of income is insufficient to enable him/her to obtain such a large amount of funds. After the National Crime Bureau and other law enforcement agencies successfully appeal to the High Court, the assets of people who fail to explain the source of their wealth may be seized and bank accounts may be frozen.

We have discussed in a previous article that many students’ bank accounts were frozen by the National Crime Agency or Police in the name of suspected money laundering due to private currency exchanges. Therefore, we once again remind students studying in the UK to use private currency exchange services carefully and not to be involved in money laundering investigations which could affect their studies. If you want to learn more about what to do if your bank account is frozen because of private exchange, you can click here to view the article.

What is Anti-Money Laundering Regulations (AML)?

Anti-money laundering legislation is a piece of legislation aimed at illegal money laundering. Money laundering refers to the illegal act of converting illegally obtained funds into legal funds or concealing the illegal source of funds. The purpose of the anti-money laundering law is to prevent money laundering activities that conceal and conceal the proceeds of crimes, such as drug crimes, organised crimes, terrorist activities, smuggling crimes, corruption and bribery crimes etc., through various means.

The process of money laundering usually includes the following 3 stages:

- Placement: Put "dirty money" into the legal financial system while hiding its source.

- Layering: This step is also known as "structuring". It hides the source of funds through a series of transactions and accounting techniques, and breaks down the funds into small transactions, making money laundering activities difficult to detect.

- Integration: After the laundered money becomes legal funds, it is withdrawn from legal accounts and real records, and then large-scale consumption, investment, etc are carried out.

In the United Kingdom, companies must abide by anti-money laundering laws. The anti-money laundering regulations in the United Kingdom stipulate that all industries that involve large amounts of capital must take a series of measures to prevent their businesses from being used for money laundering or terrorist financing purposes. For example, in the gaming industry, the UK government imposes very strict supervision. For casinos and online gambling platforms that do not have due diligence to investigate the source of customer's funds, the UK gaming regulator - the UK Gambling Commission will enforce penalties.

- In April 2020, the UK Gambling Commission (UKGC) imposed a fine of £13 million on Caesars Entertainment (now acquired by Silver Point Capital), which is the largest regulatory fine in the UK. Caesars Entertainment was punished on the grounds that it allowed a VIP registered as a high-risk gambler to place bets without investigating the source of funds, and lost £795,000. It also failed to investigate the source of funds for a lady who claimed to be a waiter and allowed her to bet £87,000. Additionally, allowed a customer to transfer £3.5 million through the casino without investigating the source and destination of funds, etc. In addition to being punished with huge fines, three senior managers of Caesars Entertainment in the UK also had their personal licenses revoked.

- March 2021, the British Gaming Corporation (UKGC) fined online casino and sports betting operator Casumo with a fine of 6 million to the Gaming Commission for anti-money laundering defaults in the United Kingdom. The casino operator must investigate the client's funds. And Casumo caused at least 5 customers to lose a huge amount of gambling money without investigating the source of customer funds.

In addition to the gambling industry, the real estate industry also involves a large amount of funds in every transaction. Therefore, the British government also urges real estate agencies and real estate transaction lawyers to check every client's funds. Especially funds from abroad, including those from areas with frequent and high-risk terrorist activities and areas with more serious bribery.

At present, the UK's anti-money laundering laws are becoming more and more stringent for financial service providers. For example, banks will always check the source of any large sum of funds in your account. If you plan to buy a house in the UK, we recommend that you prepare relevant documents and materials in advance and cooperate with a conveyancing solicitor for checking your source of funds. At the same time, we also recommend that you contact your bank manager in advance to avoid the bank from misunderstanding the large amount of money you have transferred for house purchases, which may cause your account to freeze.

If you have any questions about buying a house, investing in the UK and AML investigations, please contact us. Our team speak English, Mandarin, Cantonese, Korean, Russian, Portuguese, Spanish etc.

Account Freezing Order (AFO)

Did authorities freeze your UK bank account? Have you received notice of hearing for AFO application? Do you know what happened and what are the legal consequences?

On 28th February 2019, The UK’s National Crime Agency froze 95 Barclays’ bank accounts, mainly held by Chinese students studying in the United Kingdom. These accounts contain an estimate of £3.6 million that is suspected to be from proceeds of crime or intended to be used for criminal purposes. Accounts will be frozen for 9 months for the purpose of subsequent money laundering investigations conducted by the National Economic Crime Centre’s officer. In 2019/2020, AFOs were up to 166 cases.

Why did the authorities freeze my account?

A lot of Chinese student received letters from enforcement authorities, such as the City of London Police and the HM Revenue & Customs, confirming there was an Account Freezing Order (AFO) application against their bank accounts and a hearing was scheduled. Subsequently, these bank accounts would be frozen for nine months. These bank account users have one similarity: they frequently used Private Foreign Currency Exchange Service to exchange for pounds.

As the People’s Republic of China’s authorities implement regulations to limit the exchange of foreign currency from Renminbi, Chinese students are tempted to use Private Foreign Currency Exchange Service to exchange pounds. Chinese students perceive these private currency exchange service more convenient to use and it offers a slightly better exchange rate as incentives than banks’ service. Why not?

Private Currency Exchange Service is well-known and frequently used by the Chinese communities in the UK. These currency exchange service companies operate by sourcing Chinese customers on communications platforms such as Wechat and Alipay. The currency exchange service providers register an account on such communication platform and appear as a Universities’ alumni or some status that sounds credible in the group chat to attract Chinese customers. Chinese customers who want to use the private exchange service will simply have to contact the person they ‘met’ on the communication platform and agree with their exchange rate, the transaction can subsequently be performed. The entire private currency exchange process will take less than one day to complete while traditional currency exchange through banks may take up to 5 working days.

However, Chinese students may not know that in the United Kingdom, strict anti-money laundering regulations are enforced on banks and institutions that perform banking activities. Any large transactions and money transfers will be subject to tracing and declaration of those source of funds.

Private Foreign Currency Exchange is regulated in the United Kingdom. By violating regulations through using these Private Foreign Currency Exchange service, you might have to bear the legal consequences, often not known to you at the outset.

The New Legislation - Criminal Finance Act 2017

Since 31 January 2018, new enforcement power was introduced into the Proceeds of Crime Act 2002 by Criminal Finance Act 2017, it allows authorities to apply to Magistrates’ Court to freeze the monies in “suspicious” bank accounts or building societies account until the source of the funds can be established. Funds were either alleged to be derived from, or intended for use in, unlawful activities.

The frequent use of Private Foreign Currency Exchange services is considered one of the activities that will make Chinese Students’ bank account looks suspicious.

This is because in each transaction, the currency exchange service provider will separate the total amount of pounds into several tranches before sending. The service provider will deposit each tranche of the transaction by cash into the customer’s bank account from different bank branches all over the United Kingdom. By sending in tranches and in different branches, the service provider can avoid being suspicious when paying large amount of cash into a single account in a single branch.

When the NECC notice that there are no links between the location where cash are deposited and where the bank account holder is based, they classify this as a money laundering technique called ‘smurfing’. This constitutes a reasonable ground to suspect the source of those funds are illegitimate. Therefore, the NECC officer will subsequently apply to the Magistrates’ Court to freeze the bank account of these Chinese students for further investigations.

What are the legal consequences?

While the NECC is conducting the money laundering investigations, the account holder must cooperate with the authorities and give evidence with explanations. If the account holder fails to give evidence, the account holder may have to bear the legal consequence and sentence for money laundering. Not only the frozen funds will be forfeited, the criminal record may also affect any current and subsequent student visas in the UK.

What should I do next?

When you receive the notice of AFO applications sent by the authorities, we recommend that you seek legal advice at your earliest opportunity. The two cases set out examples of why you need to seek legal advice.

Case one:

The client’s UK bank accounts became subject to AFO. Amount frozen was over £100,000. We were instructed to communicate on the client behalf with the NCA and then help piece together the reasons for so many cash deposits to her bank accounts from different locations. Following a rigorous investigation and discussions with our client. Our ability to speak and write to our client in mandarin was crucial to her understanding what was required to explain what the transactions were. Despite good evidence to show the transactions were all accounted for, the NCA would not agree to unfreeze the bank accounts and the matter proceeded to court hearing again. Following witness evidence given by our client and a prepared bundle of documents filed with the court, the Judge refused the NCA’s request to extend the AFO and accepted our client’s funds and transactions were good. AFO discharged.

Case two:

The Client’s UK bank accounts became subject to AFO. Application brought by a police authority. Amount frozen was £30,000. The allegation was that these were proceeds of crime transfers as the cash payments were made by unknown individuals at various locations in UK. The main worry for the client was her visa status and did not want a criminal record. Following detailed discussions and thorough investigation of all transactions and transfers, we were able to persuade the police authority that only part of the frozen funds could not be accounted for. With several rounds of negotiation, it was agreed that the police would not take this further if the funds that could not be accounted for were disclaimed. A written compromise was agreed, and the client was very happy with the result.

Chan Neill solicitors is a leading Law Firm in London and we have mandarin and Cantonese speaking lawyers who are experienced in the legal area and are able to guide you through this difficult period. If you have any queries of the AFO, please do not hesitate to contact: chinadesk@cnsolicitors.com.